The European Sustainability Reporting Standards (ESRS) are poised to reshape the landscape of corporate sustainability reporting in the European Union. Having recently assisted a client with their ESRS reporting requirements, particularly the double materiality component, I have witnessed firsthand the comprehensiveness of this process. While I am a staunch advocate for robust sustainability disclosures, I am also acutely aware of the significant challenges and potential sustainability concerns this level of reporting imposes on businesses.

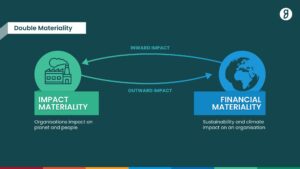

The Double Materiality Principle: A Comprehensive Approach

The ESRS’s double materiality principle, which encompasses both impact materiality and financial materiality, is particularly noteworthy. This dual approach requires companies to evaluate not only how environmental, social, and governance (ESG) factors affect their financial performance but also how their operations impact the environment and society. This thoroughness is commendable as it ensures a holistic view of sustainability, aiding companies in prioritizing key financial concerns alongside their environmental and social impacts.

However, the implementation of such an exhaustive reporting framework can be overwhelming for businesses, especially smaller enterprises that may lack the resources of larger corporations. The time-consuming nature of these disclosures raises valid concerns about their long-term feasibility and sustainability.

Paragon Impact’s Alignment with ESRS

At Paragon Impact, our impact assessment process shares many similarities with the ESRS approach. We assist clients in identifying their most material Sustainable Development Goals (SDGs), establish baselines, identify gaps and opportunities, and measure progress over time. The ESRS process aligns beautifully with this methodology, particularly with its emphasis on climate and emissions, material efficiency and waste, supply chain integrity, and social and governance aspects—key components of the broader ESG movement.

Our status as an accredited service provider with the Global Reporting Initiative (GRI) positions us well to help clients navigate these new regulations. The synergy between ESRS datasets and GRI standards enhances our ability to assist clients in building robust strategies and determining suitable metrics for future data collection. This integrated approach ensures that companies are collecting the right types of data to drive meaningful sustainability action.

Challenges and Opportunities

While the ESRS holds promise, its implementation presents significant challenges. The sheer volume of data required and the complexity of the reporting process can be daunting. Companies will need to invest in new systems and processes to comply with these standards. This is where we at Paragon Impact can play a crucial role, leveraging our expertise to simplify the reporting process and provide strategic guidance.

Despite these challenges, the ESRS represents a significant step forward in corporate accountability. The focus on both financial and impact materiality ensures that companies cannot merely pay lip service to sustainability; they must demonstrate tangible actions and outcomes. This shift from mere disclosure to actionable insights is a welcome development. As someone who has grown weary of superficial disclosures, I find this move towards accountability and action incredibly encouraging.

A Step in the Right Direction?

While the ESRS presents significant implementation challenges, its potential to drive meaningful change in corporate sustainability practices cannot be overstated. By fostering greater accountability and providing a comprehensive framework for sustainability reporting, I think the ESRS is on the right track. At Paragon Impact, we are excited to help our clients navigate this new regulatory landscape and leverage these standards to drive real, impactful change in their sustainability practices. The future of corporate sustainability reporting is here, and it’s comprehensive, challenging, and, ultimately, necessary.